For decades, retirement planning in India revolved around a simple dream — owning a home, having some savings in the bank, and living a peaceful life after work. Earlier generations often believed that even Rs 50 lakh or Rs 1 crore was enough to guarantee financial security during retirement. Today, however, that belief is rapidly changing.

Across urban India, conversations around retirement are becoming more complex, ambitious, and anxiety-driven. Many professionals now believe that even Rs 5 crore may not provide long-term financial comfort, while others estimate needing Rs 10 crore, Rs 15 crore, or even Rs 40 crore to maintain their desired lifestyle after retirement.

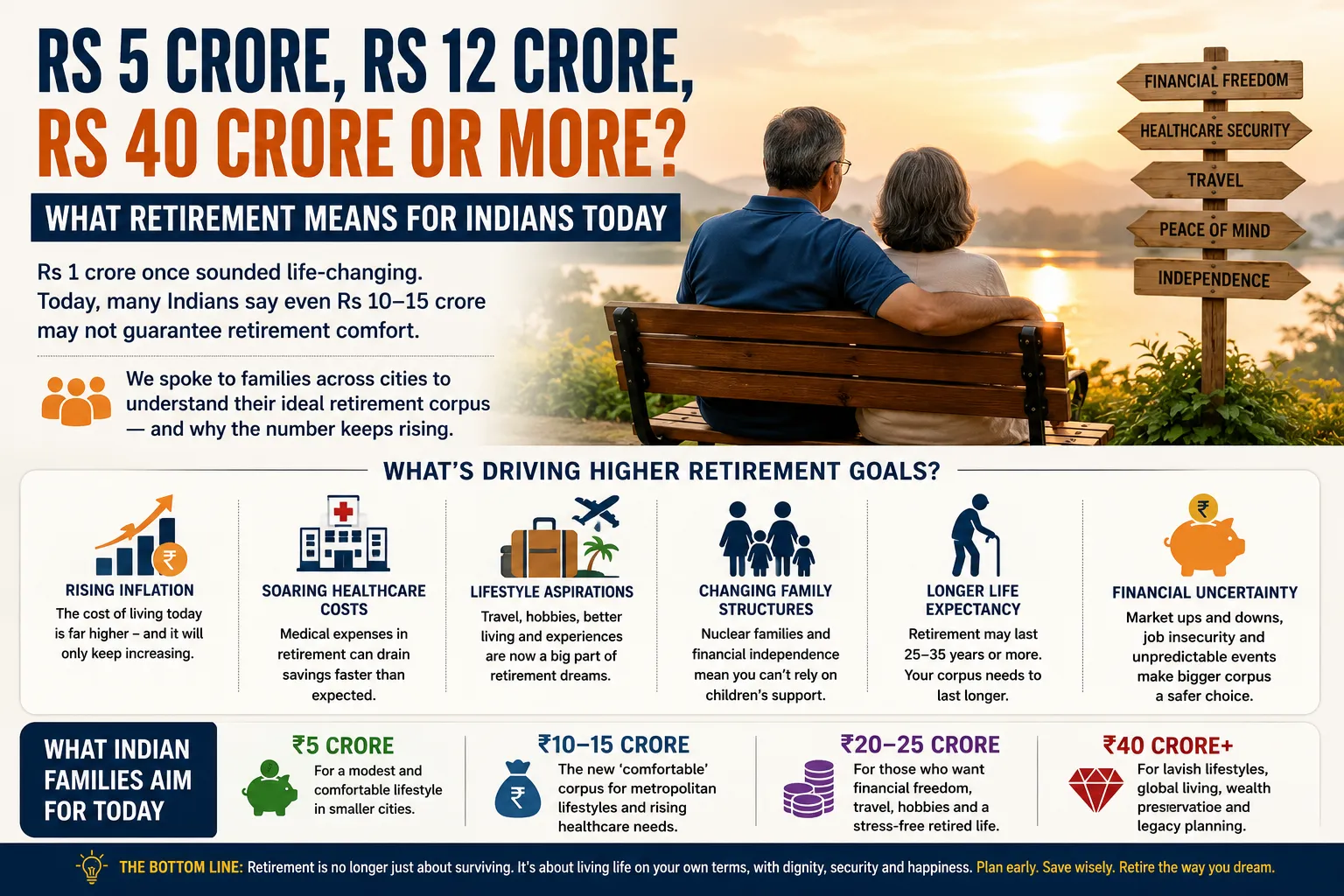

The shift reflects rising living costs, inflation, healthcare expenses, lifestyle aspirations, longer life expectancy, and changing family structures. Retirement is no longer seen merely as a period of rest. Instead, many Indians now view retirement as an extended phase of active living that includes travel, wellness, independence, hobbies, and financial freedom.

As economic realities evolve, the idea of what constitutes an “ideal retirement corpus” is undergoing a dramatic transformation.

Why Rs 1 Crore No Longer Feels Enough

There was a time when becoming a “crorepati” symbolized lifelong financial success in India. For many middle-class families, Rs 1 crore once appeared large enough to comfortably support retirement.

However, inflation and changing expenses have significantly reduced the long-term value of money.

Today’s retirees face:

-

Rising healthcare costs

-

Expensive urban living

-

Higher utility bills

-

Increasing travel expenses

-

Lifestyle inflation

-

Longer retirement years

Financial experts often point out that retirement may now last 25 to 35 years due to improved life expectancy. This means retirees need far more money than previous generations because savings must sustain them for decades.

Many urban professionals now believe Rs 1 crore may only cover basic expenses rather than provide genuine financial freedom.

The Impact of Inflation on Retirement Planning

Inflation has become one of the biggest reasons retirement targets are increasing rapidly.

Even moderate inflation significantly affects long-term purchasing power. A lifestyle that costs Rs 1 lakh per month today could require several times more money twenty years from now.

Expenses likely to rise sharply over time include:

-

Medical treatment

-

Insurance premiums

-

Housing maintenance

-

Domestic help

-

Food and utilities

-

Travel and leisure

As a result, retirement planning now requires people to think not only about current expenses but also about future economic realities.

Many families are shocked when financial calculations reveal how much money may actually be needed to maintain the same lifestyle over multiple decades.

Healthcare Costs Are Creating Major Anxiety

Healthcare has emerged as one of the biggest concerns for Indians planning retirement.

Medical inflation in India continues to rise faster than general inflation. Serious illnesses, surgeries, long-term treatments, and elderly care can quickly consume large amounts of savings.

Retirees increasingly worry about:

-

Hospitalisation costs

-

Chronic illness treatment

-

Health insurance limitations

-

Long-term care expenses

-

Emergency medical situations

Unlike earlier generations that often depended on joint family support systems, many modern retirees expect to manage healthcare expenses independently.

This financial uncertainty is pushing people to aim for much larger retirement funds than before.

Lifestyle Expectations Have Changed Dramatically

Retirement expectations today are very different from those of previous generations.

Earlier retirees often lived modestly with limited spending patterns. Modern professionals, however, aspire to maintain active and comfortable lifestyles even after leaving work.

Many people now want retirement to include:

-

Domestic and international travel

-

Dining out regularly

-

Wellness activities

-

Hobbies and passion projects

-

Financial independence

-

Comfortable housing

For some affluent urban families, retirement is no longer about “slowing down” but about finally enjoying experiences they postponed during working years.

This lifestyle shift naturally increases the amount of money people feel they need for retirement security.

The Decline of Joint Family Support

India’s social structure is also changing rapidly.

Traditional joint families once provided:

-

Shared living expenses

-

Emotional support

-

Elderly care

-

Financial backup during emergencies

Today, nuclear families have become more common, especially in urban areas.

As a result, retirees increasingly feel responsible for independently funding:

-

Healthcare

-

Housing

-

Daily living expenses

-

Emergency situations

Many elderly parents no longer assume their children will financially support them after retirement.

This growing emphasis on financial independence is encouraging people to build larger retirement corpuses.

Longer Life Expectancy Means Longer Retirement

People are living longer than previous generations due to:

-

Better healthcare

-

Improved nutrition

-

Medical advancements

-

Increased awareness about fitness

While longer life expectancy is positive, it also creates financial challenges.

A person retiring at age 60 may now need savings that last:

-

25 years

-

30 years

-

Sometimes even longer

This changes retirement calculations completely.

Retirement is no longer a short final phase of life. Instead, it has become a major life stage requiring long-term financial planning.

The fear of “outliving savings” has become one of the biggest anxieties among middle-class and upper-middle-class families.

Why Some Indians Now Target Rs 10–15 Crore

In metropolitan cities like:

-

Mumbai

-

Bengaluru

-

Delhi

-

Hyderabad

-

Pune

many professionals now estimate retirement needs in the range of Rs 10 crore to Rs 15 crore.

This number may sound extremely high, but several factors contribute to such calculations:

-

Expensive real estate

-

International education support for children

-

Healthcare inflation

-

Lifestyle maintenance

-

Travel goals

-

Investment uncertainty

People in high-income professions often want retirement lifestyles similar to their working years, which naturally requires significant wealth accumulation.

For affluent families, retirement planning increasingly includes not just survival but preserving comfort, flexibility, and dignity.

The Rise of the FIRE Movement in India

The Financial Independence, Retire Early (FIRE) movement is also influencing retirement thinking among younger Indians.

The FIRE philosophy encourages:

-

Aggressive saving

-

Early investing

-

Reduced unnecessary spending

-

Building passive income streams

Many professionals now dream of retiring in their 40s or 50s instead of working into old age.

However, early retirement requires significantly larger savings because:

-

Income stops earlier

-

Retirement lasts longer

-

Inflation affects wealth for more years

This has further increased conversations around large retirement targets like Rs 10 crore or more.

Real Estate Still Plays a Major Role

For many Indians, owning property remains central to retirement security.

People often consider:

-

Primary residence ownership

-

Rental income properties

-

Vacation homes

-

Commercial investments

as part of their retirement planning strategy.

However, rising property prices in urban India have made home ownership increasingly expensive, forcing families to allocate larger portions of savings toward housing.

Some retirees also prefer fully debt-free retirement lifestyles, which requires clearing home loans before leaving the workforce.

This further increases the amount of money people feel they need before retiring comfortably.

The Emotional Side of Retirement Planning

Retirement planning is not only financial — it is also deeply emotional.

Many professionals fear:

-

Losing financial independence

-

Becoming dependent on children

-

Facing medical emergencies alone

-

Running out of money later in life

These fears often influence retirement targets as much as actual financial calculations.

For some people, aiming for larger retirement savings provides psychological comfort and security rather than simply covering practical expenses.

The uncertainty of the future makes many families prefer “over-preparing” financially whenever possible.

Investment Awareness Has Increased

Financial literacy among urban Indians has improved significantly in recent years.

People are now more aware of:

-

Mutual funds

-

Equity investing

-

Retirement planning tools

-

SIPs (Systematic Investment Plans)

-

Compounding benefits

This increased awareness has changed how people think about long-term wealth building.

Many professionals now actively calculate future retirement needs using:

-

Inflation-adjusted projections

-

Expected returns

-

Healthcare estimates

-

Life expectancy assumptions

As a result, retirement planning discussions have become more detailed and realistic than before.

Retirement Goals Differ Across Income Groups

Not every Indian aims for retirement savings worth crores of rupees.

Retirement expectations vary greatly depending on:

-

Income level

-

City of residence

-

Lifestyle choices

-

Family responsibilities

-

Existing assets

For some families, Rs 2 crore may provide sufficient comfort, while others may genuinely require Rs 20 crore or more to sustain luxury lifestyles.

The “ideal retirement corpus” therefore depends heavily on personal goals rather than one universal number.

However, one clear trend has emerged: retirement planning is becoming more ambitious across nearly all income categories.

The Pressure of Financial Uncertainty

Global economic uncertainty is also shaping retirement attitudes.

Concerns about:

-

Market volatility

-

Job insecurity

-

Inflation

-

Economic slowdowns

-

Healthcare unpredictability

have made people more cautious and financially defensive.

Many professionals now feel they must prepare for worst-case scenarios rather than relying on optimistic assumptions.

This uncertainty is pushing retirement targets steadily upward.

Conclusion

The meaning of retirement in India is changing dramatically. What once seemed like a sufficient retirement corpus — Rs 1 crore — now feels inadequate for many urban professionals facing rising living costs, healthcare inflation, longer life expectancy, and changing lifestyle aspirations.

Today’s Indians increasingly view retirement not merely as financial survival but as a phase of independence, dignity, flexibility, and personal fulfillment. Whether the target is Rs 5 crore, Rs 12 crore, or even Rs 40 crore, the growing numbers reflect deeper anxieties and ambitions surrounding financial security in modern India.

As economic realities evolve, retirement planning is becoming more sophisticated, emotionally driven, and personalized than ever before. Ultimately, the ideal retirement corpus is no longer defined by one fixed number — it depends on the kind of life people hope to live long after their working years end.

mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao mediyao